7 Best Banks for Commercial Real Estate Loans in Utah for 2026

Utah’s commercial-real-estate market is still humming. Tech firms keep planting flags along the Wasatch Front, warehouses crowd I-15, and population growth feeds constant demand for apartments and retail.

Utah’s commercial-real-estate market is still humming. Tech firms keep planting flags along the Wasatch Front, warehouses crowd I-15, and population growth feeds constant demand for apartments and retail. At the same time, analysts expect the Federal Reserve to trim short-term rates by roughly two percentage points between late 2025 and the end of 2026, easing borrowing costs statewide—a shift Kiplinger calls “the tailwind borrowers have waited for.”

That one-two punch of strong demand and cheaper capital opens a rare window for expansion. If nine-percent pricing sank your last pro forma, seven-percent rates plus Utah’s tax-increment incentives and forty-plus Opportunity Zones could flip the math in your favor.

But terms only matter if you pair with the right lender. National banks handle nine-figure towers, credit unions stretch to ninety-percent loan-to-value for owner-occupied space, and agile community banks can wire a $3 million construction loan before a national player assigns a credit officer.

Over the next pages, we’ll sort Utah’s leading lenders into clear lanes so you can skip straight to the partners that match your size, speed, and structure. Ready to find your financing lane? Let’s dive in.

Our method: how we built the short-list

We started with numbers, not hunches. GoSBA’s 2025 data showed ninety-six active SBA lenders in Utah and $529.9 million in total 7(a) approvals, led by Zions Bank, Mountain America Credit Union, and U.S. Bank. If a lender rarely funds SBA loans, it probably won’t champion complex CRE debt.

Next, we pulled FDIC and NCUA call-report filings to verify each institution’s capital ratios, reviewed public rate sheets for current pricing and loan-to-value limits, and called local brokers to compare “street rates” with the marketing copy.

To keep the list useful, we applied four hard filters:

- Utah footprint with an active CRE or SBA desk

- At least two core CRE products (SBA, conventional, construction, bridge)

- Capital ratio above eight percent

- A clear online inquiry path or a named commercial officer

Any lender that missed even one filter was cut. The finalists fell into three natural segments (each built for a different deal size and speed): national banks, large credit unions, and agile community banks.

Bottom line: every pick ahead is data-driven, well-capitalized, and proven in Utah’s market. Let’s find the lane that fits your project.

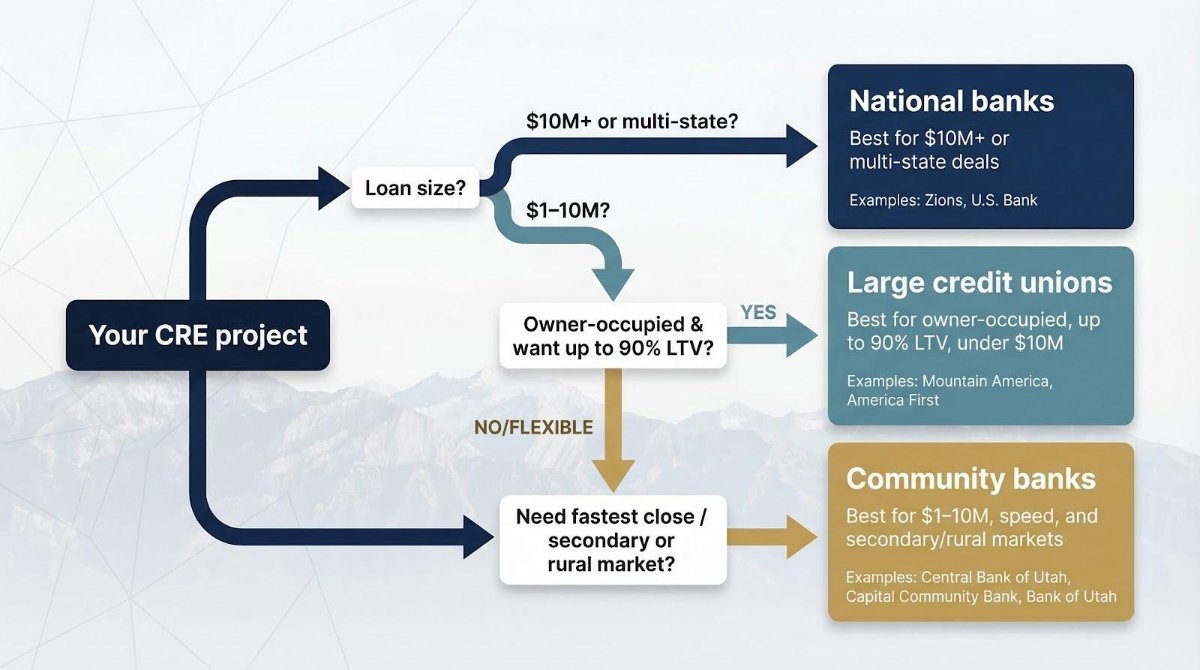

Which path fits your deal?

Before we profile individual lenders, map your project’s basics. A 75-unit apartment build in Provo needs a different balance sheet than a single-tenant office condo in Moab. Loan size, timeline, and leverage goal point you toward one of three lanes.

Picture a fork in the trail:

- National banks for deals above $10 million or projects that cross state lines.

- Large credit unions when you need up to 90 percent loan-to-value on an owner-occupied space below $10 million.

- Community banks for quick closings on $1–10 million projects, especially in secondary or rural markets.

This simple segmentation spares you from spraying applications everywhere and sets the structure for what follows: first the national players, then the powerhouse credit unions, and last the nimble hometown banks.

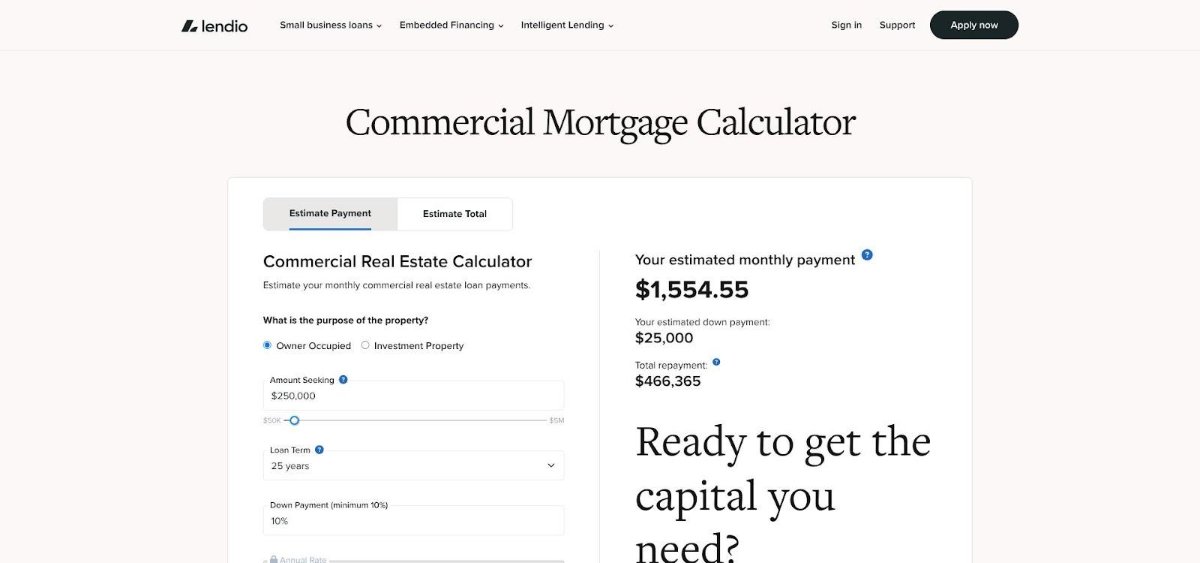

Not sure which lane your project belongs in? Commercial mortgages typically span five to twenty-five years and fall between roughly $150 000 and $5 million, ranges the Lendio commercial-mortgage calculator confirms in seconds. After you plug in your loan amount, target rate, and amortization, the Lehi-based marketplace shows an instant payment estimate and then lets you submit one short form to compare term-sheet-level quotes from more than 75 bank, credit-union, and non-bank partners, including several lenders we profile here.

Its 2024 “Best States to Start a Small Business” study shows Utah receives the highest number of SBA loan approvals per 100 000 residents—a sign that local banks and credit unions actively compete for owner-occupied real-estate deals.

Starting with a marketplace snapshot helps developers decide whether to call a national bank, a credit union, or a community lender before they sink time into full applications.

Ready to choose your lane? Let’s go.

Zions Bank: Utah’s home-grown heavyweight

If your project is above $10 million and you want a lender that already knows every zoning quirk from Ogden to St. George, start with Zions. The bank holds about $87 billion in assets and ranks first in Utah for SBA volume, evidence that it can fund everything from micro-brewery buildouts to nine-figure office towers (gosbaloans.com).

You’ll find the full toolkit here: construction draws, bridge financing, permanent loans, plus HUD and USDA programs for specialty properties. Most investor deals close around 75–80 percent loan-to-value with a minimum 1.25 debt-service ratio, while owner-occupied projects can stretch a bit higher.

Speed matters too. Credit decisions stay in Utah, so established developers often receive term sheets in days, not weeks. Combine that agility with an in-house capital-markets desk, and Zions becomes a one-stop shop whether you need a straightforward term loan or a complex syndication.

Bottom line: if scale and staying power top your checklist, Zions delivers both, along with the hometown relationships that smooth every step from appraisal to ribbon cutting.

U.S. Bank: national muscle, local touch

Need Wall Street capacity with Main Street convenience? U.S. Bank fits that sweet spot. The lender manages almost $700 billion in assets and can fund a $100 million construction line or syndicate a complex multifamily refinance. Yet its Utah commercial team keeps relationship officers in Salt Lake City, Provo, and Ogden, so you still get a direct dial when an appraisal hiccup appears.

Expect conventional terms—about 80 percent loan-to-value on stabilized properties and a 1.25 debt-service ratio—paired with pricing that tracks the tight end of the SOFR curve. The bank also wrote more than $27 million in Utah SBA loans last year, proof that it still rolls up its sleeves for smaller owner-users.

If your project crosses state lines or needs layered capital-markets work, U.S. Bank brings the breadth to keep every tranche under one roof.

Mountain America Credit Union: member-owned and rate-first

If you want lower interest costs instead of extras, Mountain America delivers. The credit union holds about $18 billion in assets yet still treats borrowers like neighbors because they are members. That structure feeds pricing: fixed commercial-mortgage rates often start a half-point below big banks, and fees stay lean.

Mountain America shines when you need up to 90 percent loan-to-value on an owner-occupied headquarters, medical condo, or light-industrial warehouse. SBA 7(a) deals move briskly here; the lender closed more than $33 million in Utah SBA volume last year, second only to Zions. Pair that record with construction-to-perm options up to $7 million and you get a flexible home for growing firms.

Speed is another perk. Because credit decisions stay in Utah, straightforward projects often reach commitment in 2 weeks. Online applications and secure document upload keep paperwork light, and loan officers visit job sites to troubleshoot draws.

The only catch is membership. You or your business must fit the credit union’s field of eligibility, usually a quick formality for Utah companies. Clear that box, and Mountain America’s mix of low rates, high leverage, and face-to-face service is tough to beat for owner-users and mid-sized developers.

America First Credit Union: low-rate choice for owner-users

America First brings the scale of a top-ten U.S. credit union—about $22 billion in assets—yet still prices loans like a neighborhood co-op. Its average SBA 7(a) rate in Utah sits below 8 percent, the lowest of any mainstream lender in the state. On a 10-year, $2 million note, that saves roughly $48 000 in interest compared with a bank quoting 10 percent.

Loan officers focus on owner-occupied real estate. You can finance up to 90 percent loan-to-value with amortizations to 30 years, ideal for firms that prefer to invest working capital in growth, not down payments. Construction loans and land acquisition deals round out the menu, generally capped near $10 million.

Service matches the pricing story. A secure online portal handles applications and document uploads, while branch bankers from Logan to St. George guide members through each draw. Because approvals ride a local credit committee, clean files often close in about 3 weeks.

The trade-off is tighter scrutiny on investor deals and ground-up multifamily. If you need maximum leverage on an apartment tower, choose another lane. But for businesses ready to buy or build their own space and pocket the rate advantage, America First is hard to beat.

Central Bank of Utah: fast-track financing for local projects

When time equals money—think a restaurant retrofit before ski season or an industrial shell that must open by July—Central Bank is rarely beaten to the closing table. Borrowers praise “local decisions made quickly” from loan officers who share the same ZIP codes as the job site, according to Central Bank of Utah’s website.

The bank targets loans between $1 million and $10 million, sweet-spotting owner-occupied offices, neighborhood retail, and light industrial pads. Expect up to 80 percent loan-to-value on stabilized properties and construction draws released at a pace set by your superintendent, not a distant committee.

Rates track Utah’s midsize-bank average—around 6.5 percent on a well-underwritten five-year fixed today—but the real edge is speed and flexibility. Need an early interest-only period to match a tenant improvement schedule? Want to pledge secondary collateral instead of a personal guarantee? Senior lenders can approve those tweaks without sending the file out of state.

Service stays personal. You still shake hands in the branch lobby, and that same banker picks up when you call about a weather delay on pour day. For developers and business owners who value local authority over corporate polish, Central Bank turns paperwork into progress.

Capital Community Bank: rural reach, personal touch

Large banks often skip Cedar City, Kanab, and other towns south of the Wasatch. Capital Community Bank steps in. With assets of about $1 billion, it backs projects local lenders grasp intuitively—motels along I-15, family restaurants near national parks, and medical offices serving Washington and Iron counties.

Loan sizes sit in the $1 million to $5 million range, too small for national credit desks yet critical for entrepreneurs outside the urban core. Up to 80 percent loan-to-value is standard on owner-occupied real estate, and the bank gladly structures SBA 504 packages through local CDC partners.

Developers praise its open-door policy. Need to adjust projections after a tourist surge? Walk in, mark up the spreadsheet with your lender, and leave with an updated term sheet. That access keeps surprises—and delays—to a minimum.

If your project lies south of Point of the Mountain and demands a lender who knows the terrain better than any spreadsheet, Capital Community Bank deserves a spot on your shortlist.

Bank of Utah: flexible financing for creative deals

Bank of Utah finishes our community-bank trio with a knack for projects that need more imagination than money. Think adaptive-reuse lofts in Ogden or a mixed-use strip where retail covers debt while townhomes build long-term value. Loan officers welcome that complexity, tailoring mini-perms, bridge lines, or SBA 504 pair-offs in a single meeting.

Most deals fall under $10 million, and underwriting allows reasonable wiggle room: loan-to-value up to 80 percent and debt-service coverage near 1.20 when collateral or sponsor strength supports it. That flexibility shortens negotiations and keeps architects, contractors, and investors working in sync.

Borrowers rave about responsiveness. Credit decisions stay in Utah, and the same banker who green-lights your term sheet can attend city council hearings if zoning questions flare up. For entrepreneurs chasing ideas outside the vanilla box, Bank of Utah moves funds—and paperwork—with refreshing creativity.

Side-by-side snapshot

Now that you have toured each lender, scan the grid below to confirm the headline numbers before you pick up the phone.

|

Lender |

Core loan types |

Max LTV* |

Min DSCR* |

Typical 5-yr fixed** |

Deal size comfort zone |

Speed note |

Signature perk |

|

Zions Bank |

SBA 7(a)/504, construction, bridge, perm |

80 % |

1.25 |

6.50–8.00 % |

$5–100 M+ |

Term sheet in days for known sponsors |

Full capital-markets desk |

|

U.S. Bank |

Conventional, HUD/FHA, SBA |

80 % |

1.25 |

6.25–7.75 % |

$10–200 M |

Digital pipeline, national credit team |

Multi-state capacity |

|

Mountain America CU |

Owner-occ, construction, SBA 7(a) |

90 % |

1.15 |

5.75–7.25 % |

$0.5–7 M |

Local committee ≈ 2 weeks |

Member pricing saves ≈ 0.50 % |

|

America First CU |

Owner-occ, land, SBA 7(a) |

90 % |

1.15 |

5.50–7.00 % |

$0.5–10 M |

Online portal, 3-week close |

State’s lowest SBA rates |

|

Central Bank of UT |

Construction, bridge, perm |

80 % |

1.20 |

6.25–7.75 % |

$1–10 M |

In-branch approval, < 3 weeks |

Rapid draws |

|

Capital Community Bank |

SBA 504, owner-occ, land |

80 % |

1.20 |

6.50–7.85 % |

$1–5 M |

Walk-in term-sheet edits |

Deep rural expertise |

|

Bank of Utah |

Bridge, mini-perm, SBA 504 |

80 % |

1.20 |

6.35–7.65 % |

$1–10 M |

Same-day structure tweaks |

Creative underwriting |

*Ranges reflect typical Utah guidelines; strong sponsors can sometimes push higher.

**Rate bands based on mid-2026 market, five-year fixed term.

Keep this chart handy. It packs ten pages of banker talk into the few numbers that drive your cash flow.

FAQs: your top loan questions answered

What is the fastest path to closing?

Community banks still win the speed game. Central Bank of Utah, for example, can issue a term sheet in days because decisions stay in state. Keep financials tight, order third-party reports early, and you could fund in about 3 weeks.

SBA 7(a) or 504—how do I choose?

Match the loan to purpose and leverage. Select 7(a) if you need working capital alongside real estate or want a single note up to $5 million. Choose 504 when you are buying or building owner-occupied property and want 90 percent financing fixed for 25 years. Both programs let you roll closing costs into the loan to conserve cash.

What loan-to-value and coverage ratios should I expect?

Utah banks cap most investor deals around 75–80 percent LTV with a 1.25 debt-service ratio. Credit unions stretch to 90 percent on owner-occupied space and may accept 1.15 coverage if your global cash flow is strong.

Are there Utah-specific incentives I can stack with my loan?

Yes. The Economic Development Tax Increment Financing (EDTIF) program can rebate up to 50 percent of new state taxes for qualifying projects, and more than 40 Opportunity Zones allow investors to defer and reduce capital-gains tax. Ask your CPA to model these before finalizing loan proceeds—you might borrow less than you expect.

Do I need to open deposit accounts to get the best rate?

Often, yes. Relationship pricing can trim 25–50 basis points when you keep operating or payroll balances with the same institution. If cash-management tech matters, test it during underwriting; switching later is tougher than renegotiating a rate.

Can I split financing between lenders?

Absolutely. Many developers pair a 504 loan for an owner-occupied headquarters with a conventional bank loan for investment property. Disclose all obligations up front so each lender can underwrite your full picture.

Bring any additional questions to your first call. A prepared borrower always secures a better deal.

Conclusion

Utah’s 2026 market rewards prepared borrowers. Once you know your deal size and speed requirements, choose the lane—national bank, large credit union, or community bank—that aligns with your goals. Reach out early, assemble documentation, and use the snapshot grid to compare terms. With rates expected to ease and demand staying strong, the right lender partnership can turn today’s blueprint into tomorrow’s ribbon cutting.

Keep reading

More from the blog

Utah vs. Florida Real Estate Markets in 2026: Key Trends

Design Details Buyers Notice During a Home Tour

How Outsourcing Improves Architectural Project Outcomes