Unlocking Homeownership: VA Loan Updates for 2025 Every Veteran Should Know

Discover the important changes to VA loans in 2025 that every veteran should know. Learn about new loan limits, no down payment advantages, and more.

The landscape of VA loans is shifting dramatically as we head into 2025. For veterans and active-duty service members aiming to own a home with zero down payment, understanding the upcoming changes is crucial. This article breaks down the significant updates and what they mean for your home-buying journey.

Introduction to VA Loan Changes

As the new year approaches, veterans and active-duty service members in Utah should prepare for significant changes to VA loans that will reshape the landscape of homeownership. With the recent announcement of increased loan limits, this is an exciting time for those looking to secure a home with the benefits of a VA loan. Understanding these changes is crucial for maximizing the potential of your VA loan benefit and navigating the home buying process effectively.

Understanding the New Loan Limits

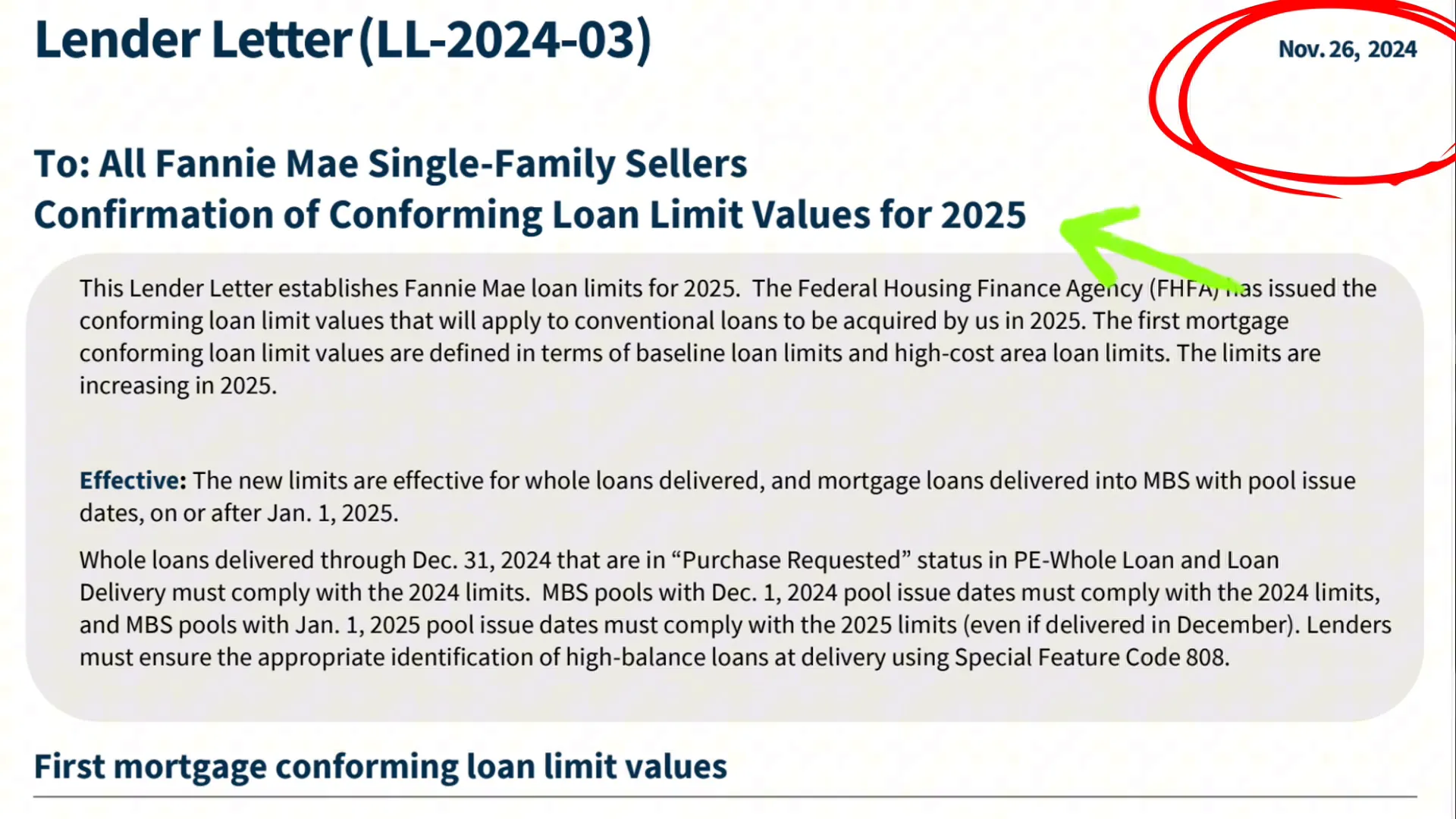

The Federal Housing Finance Agency (FHFA) has set the new conforming loan limits for 2025 at an impressive $806,500. This increase opens the door for veterans to borrow more without the burden of a down payment. For many, this change is monumental, as it alleviates a significant barrier to homeownership that has historically kept some service members from purchasing their dream homes.

It's essential to recognize that while VA loans allow for higher borrowing limits without a down payment, qualifying for the loan still requires meeting specific income and credit criteria set by lenders. This means that while the potential for homeownership has expanded, it's crucial to ensure that your financial profile aligns with lender expectations.

The Importance of No Down Payment

One of the most compelling advantages of VA loans is the opportunity to purchase a home without a down payment. This feature is particularly beneficial for veterans and active-duty service members who may not have substantial savings set aside for a traditional down payment. In many cases, this can save thousands of dollars upfront, allowing veterans to allocate their resources towards other essential expenses, such as closing costs or home renovations.

Furthermore, the absence of a down payment makes homeownership accessible to many who might otherwise be sidelined by the high cost of entry into the real estate market. This accessibility is vital in Utah's competitive housing environment, where rising property values can deter potential buyers.

Qualifying for a VA Loan

Qualifying for a VA loan involves several factors, including your credit score, income, and service history. While some lenders may accept credit scores as low as 580, a higher score generally translates to better financing terms. It is advisable for potential borrowers to focus on improving their credit scores before applying for a VA loan, as this can lead to more favorable interest rates and lower monthly payments.

In Utah, many lenders are familiar with the unique needs of veterans and can guide them through the qualification process. Understanding your financial situation and being prepared with the necessary documentation—such as W-2s, bank statements, and pay stubs—can streamline the application process and increase the likelihood of approval.

The Advantage of No Monthly PMI

Another significant benefit of VA loans is that they do not require monthly private mortgage insurance (PMI). PMI is typically mandated for conventional loans when the down payment is less than 20%. This insurance can add hundreds of dollars to a monthly mortgage payment, making homeownership less affordable over time.

By eliminating this cost, VA loans provide substantial savings for veterans, allowing them to invest more in their homes or save for future needs. Over the life of the loan, the absence of PMI can result in thousands of dollars saved, making VA loans an attractive option for many service members.

Additional Perks for Service-Connected Veterans

For veterans with service-connected disabilities, the VA loan program offers even more advantages. Specifically, those with a disability rating of at least 10% are exempt from the VA funding fee, which can be a significant cost savings. This fee is typically a percentage of the loan amount and can add up over time, but for eligible veterans, it is waived for life.

This exemption not only reduces the overall cost of the loan but also makes it easier for disabled veterans to achieve homeownership. By leveraging these benefits, service-connected veterans can better manage their finances and focus on what truly matters—creating a comfortable home for themselves and their families.

Lower Interest Rates with VA Loans

VA loans often come with lower interest rates compared to conventional and FHA loans, further enhancing their appeal. On average, veterans can expect to see savings ranging from 0.375% to 0.75% on their interest rates. This reduction can lead to significant savings in monthly payments, making homeownership more affordable in the long run.

In a state like Utah, where housing prices have been steadily increasing, these lower rates can make a substantial difference in the overall cost of buying a home. Veterans are encouraged to shop around and compare offers from different lenders to ensure they secure the best possible rate on their VA loan.

Flexibility in Property Types

The versatility of VA loans extends beyond just homeownership; they offer a diverse range of property types eligible for financing. This flexibility allows veterans and active-duty service members to choose the right property that suits their lifestyle and financial goals.

With a VA loan, you can purchase various property types including single-family homes, condos, townhomes, and multi-unit properties. This means that if you're considering house hacking—where you buy a multi-family unit and rent out a portion—you can do so with your VA loan benefits. This strategy not only helps in covering your mortgage payments but also builds your wealth over time.

Additionally, VA loans can be utilized for purchasing manufactured homes, allowing for more affordable housing options. If you're looking to create your dream home, the VA also offers options for renovation and construction financing, known as construction to permanent loans. This means you can finance the purchase of land and the building of a home all in one loan.

House Hacking and Building Wealth

House hacking is a powerful strategy for veterans looking to maximize their VA loan benefits while building wealth. By purchasing a multi-unit property, veterans can live in one unit and rent out the others, significantly reducing their monthly housing expenses. This approach not only makes homeownership more affordable but also creates a steady stream of income.

In Utah, where the housing market is competitive, this strategy can provide a substantial financial cushion. For instance, if you purchase a duplex, the rent from the second unit can cover a large portion of your mortgage payment, allowing you to invest those savings elsewhere—be it in retirement accounts, education, or additional properties.

Furthermore, house hacking can accelerate your journey towards financial independence. As property values appreciate over time, the equity built in your home can be leveraged for future investments, creating a cycle of wealth accumulation. Veterans should consider this option seriously, as it aligns perfectly with the unique advantages offered by VA loans.

Budgeting for Your Mortgage Payment

When planning to purchase a home, it is essential for veterans to establish a realistic budget for their mortgage payments. While lenders may qualify you for a certain amount based on your income and credit score, it's crucial to assess what you are comfortable spending monthly. This ensures that you do not overextend yourself financially.

A good starting point is to determine your monthly expenses and how much you can allocate towards housing. For example, if your goal is to keep your monthly payment around $2,200, it's wise to reverse engineer that figure to understand the corresponding purchase price. This strategy helps in setting clear financial boundaries and promotes a sustainable homeownership experience.

Additionally, consider other costs associated with homeownership, such as property taxes, insurance, maintenance, and HOA fees, if applicable. By factoring in these expenses, veterans can develop a comprehensive budget that aligns with their financial capabilities and long-term goals.

Loan Terms and Refinancing Options

VA loans offer flexible loan terms, ranging from 15 to 30 years, allowing veterans to choose a plan that best suits their financial situation. Shorter loan terms, such as 15 years, can lead to significant savings on interest and help build equity faster, while longer terms may provide lower monthly payments, easing financial pressure.

In addition to purchasing a home, veterans should also be aware of refinancing options available through VA loans. The VA Interest Rate Reduction Refinance Loan (IRRRL) is a streamlined option that allows veterans to refinance their existing VA loans with minimal documentation and no appraisal. This is particularly beneficial when interest rates drop, as it can lower monthly payments and overall loan costs.

Another option is the cash-out refinance, which allows veterans to tap into their home's equity for various purposes, such as home improvements or consolidating high-interest debt. This flexibility can be a game-changer for managing finances and investing in future opportunities.

Required Documents for VA Loans

When applying for a VA loan, having the right documentation ready is crucial for a smooth application process. Commonly required documents include W-2 forms, bank statements, pay stubs, and a valid photo ID. Veterans should also be prepared to provide their Certificate of Eligibility (COE), which verifies their entitlement to VA loan benefits.

Being organized and having these documents readily available can expedite the approval process. It's advisable to consult with a mortgage professional who specializes in VA loans to ensure that all necessary paperwork is complete and accurate. This preparation can save time and reduce stress during the home buying journey.

Conclusion and Final Thoughts

The changes to VA loans in 2025 present an exciting opportunity for veterans and active-duty service members looking to achieve homeownership with favorable terms. With increased loan limits, flexibility in property types, and the absence of monthly PMI, the VA loan program remains one of the most beneficial financing options available.

By understanding how to leverage these benefits, veterans can navigate the home buying process with confidence and make informed decisions that align with their financial goals. Whether it's through house hacking, refinancing, or selecting the right loan terms, there are numerous strategies to maximize the value of your VA loan.

For more resources and information on navigating the Utah real estate market, visit Best Utah Real Estate.

Frequently Asked Questions

1. What is the maximum loan amount I can borrow with a VA loan in 2025?

The conforming loan limit for VA loans in 2025 is set at $806,500, allowing veterans to purchase homes without a down payment up to this amount.

2. Do I need a down payment for a VA loan?

No, one of the significant advantages of VA loans is that they do not require a down payment, making homeownership more accessible for veterans.

3. Can I use a VA loan for investment properties?

Yes, VA loans can be used for multi-unit properties where you can live in one unit and rent out the others, making it a viable option for investment.

4. What documents do I need to apply for a VA loan?

Common documents include W-2s, bank statements, pay stubs, photo ID, and the Certificate of Eligibility (COE).

Posted by Kristopher Larson

Related Articles:

Frequently asked questions

What is the maximum loan amount I can borrow with a VA loan in 2025?

Do I need a down payment for a VA loan?

Can I use a VA loan for investment properties?

What documents do I need to apply for a VA loan?

Keep reading

More from the blog

Utah vs. Florida Real Estate Markets in 2026: Key Trends

Design Details Buyers Notice During a Home Tour

How Outsourcing Improves Architectural Project Outcomes